")

")

For many graduate students, pursuing higher education often comes with the burden of student loan debt. As you prepare to graduate from graduate school, understanding your student loan repayment options is crucial for managing your finances and planning for the future. In this blog post, we’ll explore the various student loan repayment options available to graduate students and provide guidance on choosing the right repayment plan to fit your financial circumstances and goals.

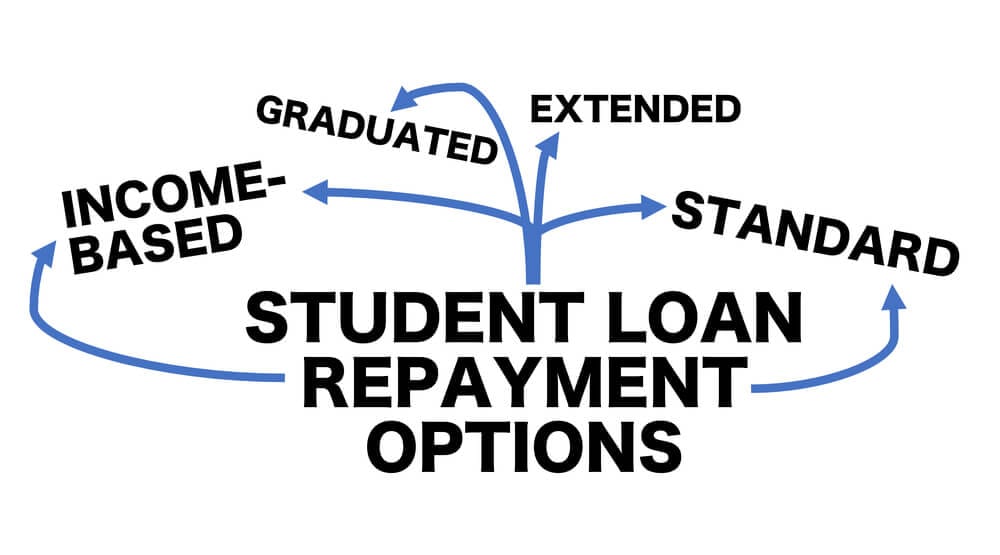

- Federal Student Loan Repayment Plans: Federal student loans offer several repayment plans tailored to meet the needs of borrowers with varying financial situations. These repayment plans include:

- Standard Repayment Plan: Under this plan, you’ll make fixed monthly payments over a 10-year term. While this plan typically results in higher monthly payments, it allows you to pay off your loans more quickly and minimize total interest costs.

- Graduated Repayment Plan: With this plan, your monthly payments start lower and increase every two years over a 10-year term. This option may be suitable if you expect your income to increase steadily over time.

- Income-Driven Repayment Plans: Income-driven repayment plans such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), and Income-Contingent Repayment (ICR) cap your monthly payments at a percentage of your discretionary income and extend the repayment term to 20 or 25 years. These plans are ideal for borrowers with low income relative to their student loan debt.

- Loan Forgiveness and Discharge Programs: Graduate students may qualify for loan forgiveness or discharge programs that forgive or discharge a portion or all of their federal student loans under certain circumstances. These programs include:

- Public Service Loan Forgiveness (PSLF): PSLF forgives the remaining balance on your Direct Loans after you’ve made 120 qualifying monthly payments while working full-time for a qualifying employer in public service or nonprofit sectors.

- Teacher Loan Forgiveness: This program forgives up to $17,500 of your Direct or FFEL Loans after you’ve taught full-time for five consecutive years in a low-income school or educational service agency.

- Total and Permanent Disability Discharge: If you’re unable to work due to a total and permanent disability, you may qualify for a discharge of your federal student loans.

- Private Student Loan Repayment Options: If you have private student loans for graduate school, repayment options and terms may vary depending on the lender. Contact your loan servicer to discuss repayment options such as fixed or variable interest rates, graduated repayment, or extended repayment terms. Some lenders may offer hardship or forbearance options if you’re facing financial difficulties.

- Refinancing and Consolidation: Refinancing or consolidating your student loans can help streamline your repayment process and potentially lower your interest rate. Refinancing involves replacing your existing loans with a new loan from a private lender with a lower interest rate and/or more favorable terms. Consolidation combines multiple federal student loans into a single loan with a fixed interest rate and extended repayment term, simplifying your repayment and reducing your monthly payments.

Conclusion: As you prepare to repay your student loans after graduate school, it’s essential to explore and understand your repayment options to make informed decisions about managing your debt effectively. Consider factors such as your income, expenses, career goals, and eligibility for forgiveness or discharge programs when choosing a repayment plan. Don’t hesitate to contact your loan servicer or financial aid office for personalized guidance and assistance in navigating the student loan repayment process. With careful planning and proactive management, you can successfully repay your student loans and achieve financial stability as you embark on your post-graduate journey.